Welcome to the Retail Times website

Enjoy your free access to all the news, featured articles and content from our sponsors.

See here for an overview of all of the retail news

Enjoy your free access to all the news, featured articles and content from our sponsors.

See here for an overview of all of the retail news

Today, Klarna, the AI-powered global payments provider and shopping assistant, released ‘The Untrend Report’, a look into the top products...

It’s coming home! Lidl are helping to kick-off the excitement for UEFA EURO 2024™ this year by offering 22 Lidl...

Live events and communications agency Meet & Potato in collaboration with Butlin’s put on The Greatest Show in Town for...

Diversified Communications, organiser of Seafood Expo Global/Seafood Processing Global, the largest and most diverse seafood trade event in the world,...

pladis, the global snacking company behind some of the UK’s most loved and iconic brands, is building on the success...

Materials science company PANGAIA is set to open its first standalone UK flagship store in Shaftesbury Capital’s Soho neighbourhood, in...

JD has opened a global flagship store on the world-renowned Avenue des Champs-Élysées in Paris, with a grand opening to...

Perfetti Van Melle, the world’s second leading confectionery manufacturer, is targeting the growing sharing opportunity and a younger audience with...

Mint Velvet, the British womenswear brand renowned for its relaxed yet glamorous style, has announced it will open a key...

Grind’s speciality coffee will be available in Tesco stores across the UK, furthering the company’s mission to bring sustainable, great-tasting...

Small independent restaurants in London and Manchester can now apply for a share of £220,000 to help grow their business...

Warburtons has launched Gluten Free Pittas in stores nationwide. These fluffy, flavourful pittas are convenient, versatile, and reviving the gluten-free...

Pret A Manger, the freshly handmade food and organic coffee shop, has revealed its spring menu featuring a mixture of...

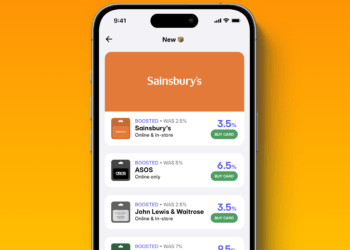

The largest bank-powered rewards app in the UK, Cheddar, has expanded its category of partners across grocery and fashion -...

As the nation gears up for the UK’s biggest running race in London, Deliveroo has teamed up with Boots to...

The tables have turned on traditional first anniversary gifts, with PizzaExpress choosing to mark the one-year milestone of their successful...

Despite the Government refusing to overturn the abolition of the duty-free shopping for tourists in the Spring Budget, now half...

The UK is undoubtedly a nation of tea lovers, with over 100 million cups drunk each day! To celebrate, new data from TonerGiant has...

UK bed specialist, Bensons for Beds has today announced the appointment of Mark Slater as chief commercial officer. The role...

bp has announced it is continuing to invest in the security of its retail team members by rolling out the...